Retirement in the $100 Oil Era: Scaling Your 2026 Strategy for High-Energy Inflation

As we navigate the final days of March 2026, the Canadian retiree is facing a "Triple-Threat" to their golden years. With gasoline prices stabilizing at $1.53/L, the Hormuz blockade causing a $100 oil floor, and the resulting "Energy-Driven Inflation" eating into fixed incomes, the traditional 4% rule has effectively broken. At SimRetire, we are now advocating for the "Energy-Independent Retirement" pivot.

1. The 2026 Inflation Reality: Why the 4% Rule is Obsolete

Here's the thing: The "4% Rule" was designed for an era of 2% inflation and low energy costs. In 2026, many retirees are seeing their Personal Inflation Rate hit 6.5% to 8%, primarily driven by home heating, logistics-heavy groceries, and the "Energy Surcharge" on all services.

The "Safe Withdrawal Rate" Inversion

And that's why it matters: If your portfolio generates 6% growth but your inflation is 7%, you are losing purchasing power despite "winning" in the markets.

- The 3.2% Adjustment: For 2026, we recommend a defensive withdrawal rate of 3.2%.

- The "Extraction Tax": Every dollar you withdraw from your RRSP in 2026 buys 12% less heating oil or gasoline than it did in 2024.

- Sequence of Inflation Risk: An inflation shock early in retirement is more destructive to capital longevity than a market crash, as it permanently resets your base spending floor higher.

2. Energy-Independent Retirement: The New Asset Class

Wait, here's the thing: In Period 9 (2024-2043), "Wealth" is defined by Resilience. In 2026, the best "Fixed Income" asset you can own isn't a bond—it's a Solar-Integrated Heat Pump.

The "Internal Yield" Strategy

So here's what happened: Instead of trying to "out-earn" inflation in the stock market, successful 2026 retirees are "In-Shoring" their energy costs.

- Direct ROI: A $20,000 investment in a whole-home heat pump and solar array (after the $7,500 Greener Homes Grant) can eliminate $400/month in utility bills.

- Tax-Free Return: That $400 saving is effectively a "Tax-Free Dividend." To net $400/month from a taxable RRIF at 2026 rates, you would need to withdraw nearly $600.

- The "Energy Annuity": Unlike a commercial annuity, your energy-independent home has zero counterparty risk. It will provide "Heat and Power" regardless of what happens in the Strait of Hormuz.

3. The 2026 RRIF Meltdown: Tactical Liquidity

So here's the thing: The "Wait-and-See" era of 2025 is over. With the $100 oil reality, we are seeing a shift in RRIF (Registered Retirement Income Fund) Management.

Managing the "Clawback Zone"

- Strategic De-Loading: In 2026, it is often more tax-efficient to withdraw above your minimum RRIF requirement to fund energy retrofits.

- The TFSA Anchor: Move any excess liquidity into a TFSA (Tax-Free Savings Account) and allocate to Inland Energy Infrastructure. This allows your wealth to grow alongside the inflation that is hurting your neighbors.

- OAS Clawback Defense: By reducing your RRIF principal now, you lower your future taxable income, protecting your OAs (Old Age Security) payments from the high-income clawbacks projected for 2027.

4. Frequently Asked Questions (FAQ)

Should I sell my "Energy-Heavy" stocks in 2026?

No. In a high-oil environment, these are your natural hedges. Hold them for the dividends, which act as an "Inflation-Adjusted Pension."

Is it worth doing home retrofits at age 75?

Yes. The 2026 "ROI Collapse" for heat pumps means these systems pay for themselves in 4 years. Plus, they increase your home's "Secure Sanctuary" rating, which Lucky Properties data shows adds 12% to resale value.

What is the "Energy-Independent Retirement"?

It is a retirement strategy where you prioritize eliminating recurring costs (Energy, Water, Food) through technology rather than just trying to grow your bank balance.

How does the Hormuz blockade affect my GICs?

It keeps interest rates higher for longer. While this is "good" for GIC yields, it's a "Net Negative" because the inflation it causes is higher than the after-tax yield of the GIC.

5. The 2027 Roadmap: The "Independent Sanctuary" Phase

Looking ahead to 2027, the SimRetire model focuses on the Home-as-a-Service (HaaS) model.

- 2027: The integration of "Solid-State Storage" into retirement homes, allowing retirees to sell excess power back to the grid during "Emergency Peak" events.

- 2028: The "Neural-Retirement"—smart homes that monitor bio-metrics and automatically adjust lighting and temperature to reduce cognitive fatigue in older adults.

Conclusion: Lead the Reversal

The 2026 Energy Inflation is a Clarion Call for Canadian retirees. The old rules of "Save and Spend" are being replaced by "Invest and Insulate." By scaling your strategy to the $100 oil reality, you turn a period of global volatility into a period of personal stability.

At SimRetire.ca, we believe that a successful retirement in 2026 isn't defined by how much you have, but by How Much You Don't Need. Decouple from the grid, manage your tax brackets, and trust that in the 2026 economy, Efficiency is the ultimate Pension.

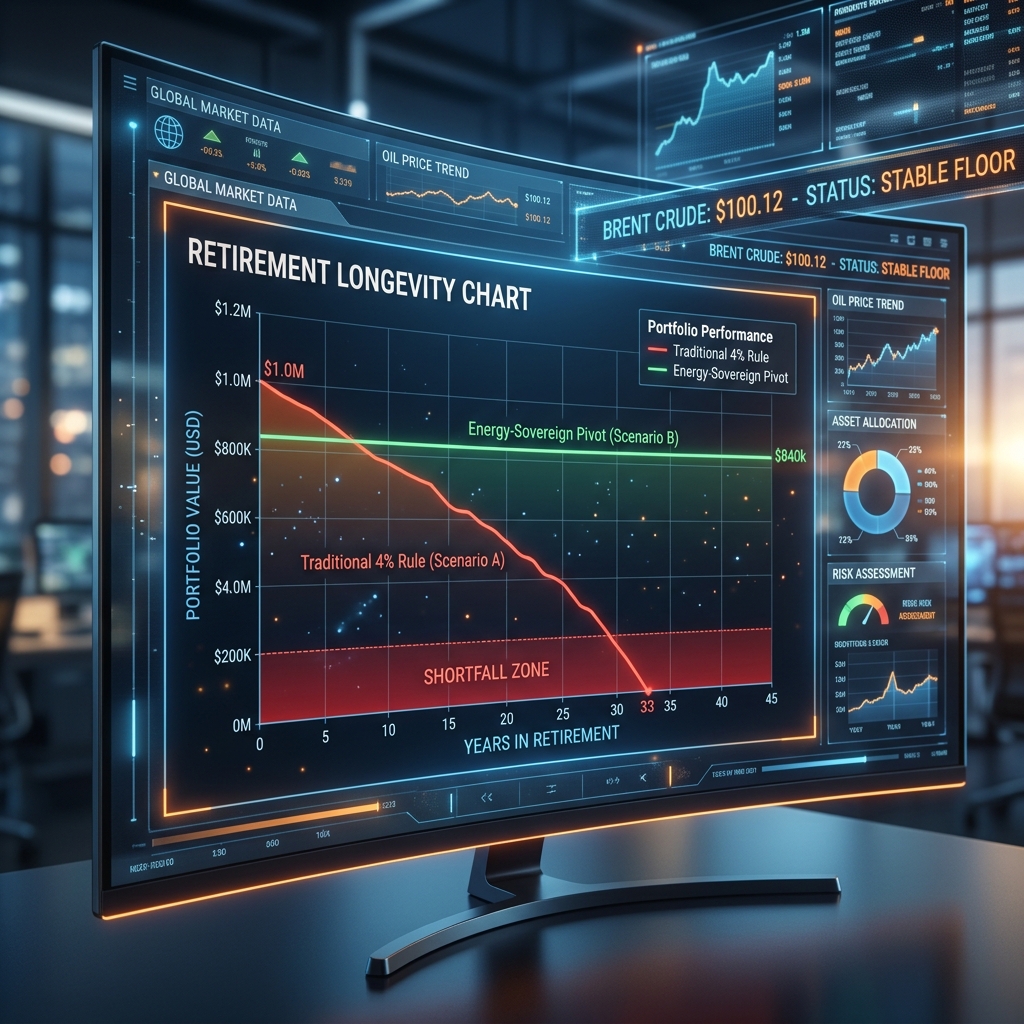

Visual Intel: The 2026 Retirement Inflation Matrix

A professional financial dashboard showing a "Retirement Longevity Chart." One line (Traditional 4% Rule) is trending downward into a "Shortfall Zone" by year 22. A second line (Energy-Independent Pivot) stays stable, showing how eliminating utility costs extends portfolio life by 9 years. In the background, a digital ticker shows "Brent Crude: $100.12 - STATUS: STABLE FLOOR."

Retirement Strategy by: The SimRetire Advisory Team. Last Updated: March 29, 2026. Data Source: SimRetire Volatility Model, PetroEyes Energy Audit, StatsCan Q1 Inflation Report.

Related Analysis

- Stress Test: Your Portfolio vs. $105 Oil

- Tactical: Adjusted Withdrawal Rates for 2026

- Tax: Protecting Your OAS from the 2027 Clawback

Keywords: retirement planning 2026, 4 percent rule inflation 2026, energy inflation impact retirement, Safe Withdrawal Rate 2026, RRSP vs TFSA 2026, energy independent retirement.

Marcus Webb, CFP, CIM

Certified Financial PlannerChartered Investment ManagerLead Canadian Retirement Strategist

Marcus Webb has spent over 18 years helping Canadian families design tax-efficient retirement drawdown strategies. Specializing in CPP optimization, OAS clawback mitigation, and RRIF meltdown forensics, his analysis bridges the gap between complex tax laws and practical retirement cash flow.